Welcome to the world of creditors, where you hold the key to unlocking debts owed to you. As a creditor, you are the person or business to whom liabilities are owed. With rights and responsibilities, you play a vital role in managing risk, seeking legal remedies, and strategizing debt collection. This article will delve into the intricacies of maintaining healthy relationships with debtors and the impact of technology on creditor-debtor dynamics. Join us on this journey and discover the power of being a creditor.

Key Takeaways

- Creditors are individuals or businesses that lend money or extend credit to others.

- Creditors have the responsibility to assess creditworthiness, determine loan terms, and monitor debt repayment.

- Different types of liabilities owed to creditors include accounts payable, loans, and credit card debt.

- Proper management of liabilities owed to creditors is crucial for financial health and can impact credit scores and future financial opportunities.

The Definition of a Creditor

As a creditor, you play a crucial role in lending money and extending credit to others. A creditor is defined as a person or business to whom a liability is owed. When you lend money or extend credit, you become the creditor, and the borrower becomes the debtor. Your role as a creditor is to assess the creditworthiness of the borrower, determine the terms of the loan or credit extension, and monitor the repayment of the debt.

It is essential to maintain accurate records of the amounts owed, the repayment schedules, and any interest or fees charged. Understanding the responsibilities and risks associated with being a creditor is crucial in managing your lending activities effectively. Now, let’s explore the different types of liabilities owed to creditors.

Types of Liabilities Owed to Creditors

When it comes to liabilities owed to creditors, there are several types to consider. These can include accounts payable, loans, and credit card debt. Each type of liability carries its own set of rights and responsibilities for both the creditor and the debtor, and understanding these can greatly impact your financial health.

Creditor Rights and Responsibilities

You have certain rights and responsibilities as a creditor. As a creditor, you have the right to be repaid the money owed to you by the debtor. This means that you have the power to take legal action to recover the debt, such as filing a lawsuit or garnishing wages. However, you also have the responsibility to treat the debtor fairly and respect their rights.

This includes not using abusive or harassing tactics to collect the debt and providing accurate information about the debt. It is important to understand the laws and regulations that govern debt collection to ensure that you are acting within the boundaries of the law. By fulfilling your rights and responsibilities as a creditor, you can maintain a respectful and fair relationship with the debtor.

Impact on Financial Health

Understanding the impact on your financial health is crucial when managing your creditor rights and responsibilities. As a borrower, it is essential to recognize that your financial well-being can be significantly influenced by how you handle your debts and obligations. When you default on payments or fail to meet your responsibilities, it can negatively affect your credit score, making it harder for you to obtain future loans or credit.

Additionally, late fees and penalties can accumulate, further burdening your financial situation. On the other hand, responsibly managing your creditor rights can have a positive impact on your financial health. Timely payments and fulfilling your obligations can help improve your credit score and open doors for better financial opportunities. It is important to be aware of these potential consequences and make informed decisions to safeguard your financial well-being.

Rights and Responsibilities of Creditors

As a creditor, it’s important to be aware of your rights and responsibilities. Being knowledgeable about these aspects can help you navigate the complex world of lending and ensure that your interests are protected. One of your key rights as a creditor is the right to receive timely payments from the debtor. This means that the debtor has an obligation to pay back the borrowed amount along with any agreed-upon interest or fees within the specified time frame.

On the other hand, as a creditor, you have a responsibility to provide accurate and transparent information to the debtor about the terms and conditions of the credit agreement. This includes disclosing the interest rate, payment schedule, and any additional charges. By understanding and fulfilling your rights and responsibilities, you can maintain a healthy and mutually beneficial relationship with your debtors, fostering a sense of belonging and trust in the financial community.

How Creditors Assess and Manage Risk

When assessing and managing risk, creditors employ various methods to ensure the safety of their investments. As a creditor, you must carefully evaluate the financial stability and creditworthiness of potential borrowers. By analyzing credit reports, financial statements, and other relevant information, you can determine the likelihood of default and adjust lending terms accordingly. Additionally, effective risk management strategies, such as diversifying your loan portfolio and setting appropriate interest rates, can help mitigate potential losses and protect your assets.

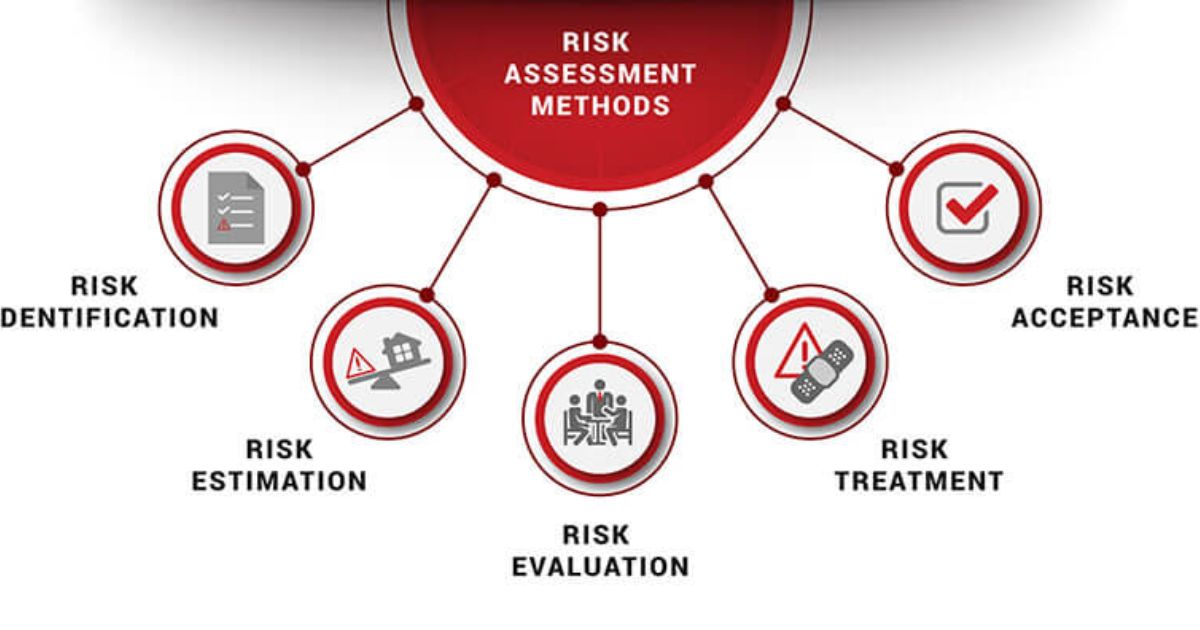

Risk Assessment Methods

You should consider using risk assessment methods to evaluate the liabilities owed to you. By utilizing these methods, you can gain a deeper understanding of the potential risks associated with your creditors and make informed decisions to mitigate them. One effective way to conduct risk assessment is by using a risk matrix, which evaluates the likelihood and impact of each risk.

Another method is the Monte Carlo simulation, which uses probability distributions to analyze the range of possible outcomes. Additionally, financial ratio analysis can provide valuable insights into the financial health and stability of your creditors. By incorporating these risk assessment methods into your evaluation process, you can effectively manage your liabilities and minimize potential risks.

| Risk Assessment Methods |

|---|

| Risk Matrix |

| Monte Carlo Simulation |

| Financial Ratio Analysis |

Creditors’ Risk Management

To effectively manage potential risks from your creditors, it’s essential to implement proper risk management strategies. Creditors play a crucial role in your financial health, and understanding how to manage the risks associated with them can help protect your interests. Here are some key strategies to consider:

- **Maintain a good credit history:** Pay your bills on time and avoid defaulting on any loans or credit obligations.

- **Diversify your sources of credit:** Relying on a single creditor can increase your vulnerability. Seek credit from different sources to spread the risk.

- **Monitor your credit utilization:** Keep your credit utilization ratio below 30% to demonstrate responsible borrowing behavior.

- **Regularly review creditor agreements:** Stay informed about the terms and conditions of your agreements to ensure compliance and identify any potential risks.

- **Establish open communication:** Maintain a positive relationship with your creditors by communicating openly and proactively addressing any issues or concerns.

Reducing Creditor Liability

To reduce the risk of liability to your creditors, it’s important to carefully review and understand any contractual agreements you enter into. By doing so, you can ensure that you are aware of your obligations and can fulfill them accordingly. This will not only protect your business interests but also establish a sense of trust and credibility with your creditors.

It is crucial to maintain open lines of communication with your creditors, keeping them informed of any changes or challenges that may affect your ability to meet your obligations. By being proactive and transparent, you can foster a positive relationship with your creditors and potentially negotiate more favorable terms if needed. This commitment to managing your creditor relationships responsibly can greatly reduce the risk of liability and help you maintain financial stability. As such, it is important to understand the legal remedies available to creditors in case of default or non-payment.

Legal Remedies for Creditors

As a creditor, your legal remedies may include filing a lawsuit to recover the debt owed to you. This is a common course of action for creditors seeking to enforce their rights and collect what is owed to them. Here are some important legal remedies available to you as a creditor:

- **Obtaining a judgment**: If you successfully win your lawsuit, the court can enter a judgment in your favor, which legally establishes the debt owed to you.

- **Garnishment**: This allows you to collect the debt directly from the debtor’s wages or bank account.

- **Seizing assets**: In some cases, you may be able to seize and sell the debtor’s property to satisfy the debt.

- **Placing a lien**: By placing a lien on the debtor’s property, you can ensure that you are paid before they can sell or transfer it.

- **Negotiating a settlement**: Instead of going through a lengthy legal process, you can negotiate a settlement with the debtor to resolve the debt.

These legal remedies provide you with options to pursue the recovery of your debt, ensuring that your rights as a creditor are protected.

Strategies for Debt Collection

If you’re looking to collect a debt, it’s important to consider effective strategies for debt collection. One approach is to start with a friendly reminder, using a respectful tone and empathizing with the debtor’s situation. This can help maintain a positive relationship and increase the likelihood of payment. If the debtor fails to respond, you may need to escalate the collection process by sending a formal demand letter or engaging a collection agency.

It’s crucial to keep accurate records of all communication and follow legal guidelines to avoid any potential legal issues. Remember, maintaining a healthy relationship between debtors and creditors is essential for long-term success. By implementing these strategies, you can increase your chances of recovering the debt while preserving a positive connection with your debtors.

Maintaining a Healthy Relationship Between Debtors and Creditors

When maintaining a healthy relationship between debtors and creditors, it’s important to communicate openly and address any concerns promptly. This ensures that both parties are on the same page and can work together towards resolving any outstanding debts. To foster a positive relationship, consider the following:

- **Establish clear payment terms**: Clearly define the terms and conditions of the debt, including due dates and payment methods.

- **Regularly communicate**: Keep the lines of communication open, providing updates on payment status and addressing any issues or concerns promptly.

- **Be understanding**: Show empathy towards debtors who may be facing financial difficulties and work together to find mutually beneficial solutions.

- **Offer flexibility**: Consider offering flexible payment options or negotiating alternative arrangements to help debtors meet their obligations.

- **Maintain professionalism**: Keep interactions respectful and professional, even in challenging situations, to foster trust and mutual respect.

The Impact of Technology on Creditor-Debtor Relationships

Technology has greatly influenced the relationship between creditors and debtors, allowing for more efficient communication and streamlined payment processes. With the advent of online platforms and digital payment systems, debtors can now easily make payments, set up automatic transfers, and track their payment history in real-time. This level of convenience not only benefits debtors but also enhances the overall efficiency of the creditor-debtor relationship.

Additionally, technology has provided creditors with tools to automate the debt collection process, reducing the need for manual intervention and saving time and resources. By leveraging technology, creditors can now send automated reminders, generate payment schedules, and even negotiate payment terms electronically. This improved communication and accessibility foster a sense of belonging and trust between creditors and debtors, ultimately leading to healthier and more productive relationships.

Frequently Asked Questions

Can a Creditor Refuse to Provide Credit to a Debtor Based on Personal Reasons?

A creditor can refuse to provide credit to a debtor based on personal reasons, as long as it doesn’t violate any anti-discrimination laws. However, it’s important for creditors to be fair and consistent in their decision-making process to avoid legal issues.

How Can a Creditor Protect Their Rights if a Debtor Declares Bankruptcy?

To protect your rights as a creditor when a debtor declares bankruptcy, you can file a proof of claim, attend meetings of creditors, and participate in the bankruptcy proceedings. This ensures you have a voice and can potentially recover some of your owed debt.

Are There Any Legal Limitations on the Interest Rates a Creditor Can Charge a Debtor?

Yes, there are legal limitations on the interest rates a creditor can charge you, as a debtor. These limitations vary depending on the jurisdiction and type of loan, ensuring fair and reasonable terms.

What Actions Can a Creditor Take if a Debtor Fails to Make Timely Payments?

If a debtor fails to make timely payments, a creditor can take legal action. They may initiate a lawsuit, obtain a judgment, and seek to collect the debt through methods such as wage garnishment or seizing assets.

How Does a Creditor Assess the Creditworthiness of a Potential Debtor Before Extending Credit?

To assess the creditworthiness of a potential debtor, creditors analyze various factors such as credit history, income stability, and debt-to-income ratio. This helps them determine the likelihood of the person/business being able to repay the debt.

Conclusion

In conclusion, as a creditor, it is essential to understand your rights, responsibilities, and the strategies for debt collection. While some may argue that maintaining a healthy relationship between debtors and creditors is challenging, it is crucial to overcome this objection by embracing technology’s impact on creditor-debtor relationships. By leveraging technological advancements, creditors can streamline processes, improve communication, and ultimately enhance the efficiency and effectiveness of their debt collection efforts. Stay informed, adapt to change, and build a strong foundation for successful creditor-debtor relationships.